FX ecosystem 03 | Liquidity benefits: Do (not) settle for less | ShapingFX series

For decades, the mitigation of settlement risk in the FX market has been high on the agenda of both public policy makers and the industry. With the advent of the CLS settlement service in September 2002, an effective mechanism for FX settlement risk mitigation quickly became the de facto market standard.¹ But CLS offers much more than risk mitigation – it provides an efficient flow of liquidity and delivers significant operational benefits.

The trade-off between risk reduction and liquidity efficiency in payments

Interbank payment systems are the backbone of the financial sector. In most of today’s systems, payments are transferred from sender to receiver on a transaction-by-transaction basis,2 which is considered the most effective way to mitigate settlement risk. By construction, sufficient liquidity needs to be available in these real-time gross settlement (RTGS) systems.3 In a nutshell, liquidity greases the wheels of payment processing engines.

Liquidity in payment systems is provided through available funds or intraday credit lines.4 If liquidity is not available and credit lines cannot be used, market participants must borrow from central banks or other banks via the money market.

If liquidity is sitting idle on payment system accounts, it cannot earn interest elsewhere and thus incurs an opportunity cost, the size of which depends on the applicable interest rate. Therefore, payment systems often provide sophisticated liquidity-saving mechanisms to their users.5

As an interbank settlement system, CLSSettlement is no exception to this trade-off between risk reduction and liquidity efficiency. CLS was established by the private sector in response to a public sector call to address FX settlement risk on a global scale. Settlement risk could materialize if payment instructions for the two currency legs of an FX trade are not settled at the same time, which can result in one party to the FX trade paying in one currency but not getting paid in the counter currency.

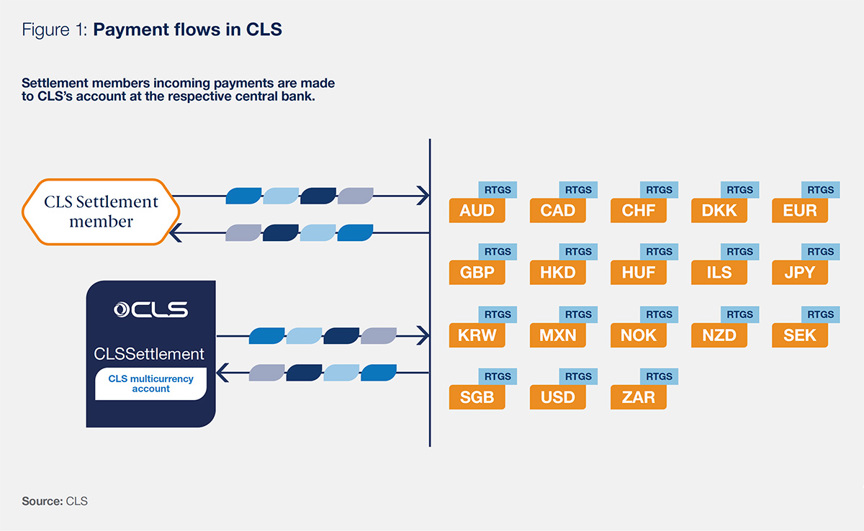

CLS mitigates FX settlement risk by providing a payment-versus-payment (PvP) service, CLSSettlement, in which the payments on both sides of an FX trade are settled simultaneously. It offers a unique arrangement for 18 of the world’s most actively traded currencies: by holding accounts with the central bank of each currency, CLS can make and receive payments via the RTGS systems of the respective central banks (Figure 1). Like other interbank payment systems, CLS provides liquidity-saving tools to reduce strains on liquidity. What distinguishes CLS from many other payment systems is the magnitude of liquidity efficiency it provides.

1See Shaping FX series, whitepapers 01 and 02; cls-group.com/insights/2Committee on Payments and Market Infrastructures (CPMI) – A glossary of terms used in payments and settlement systems. 3Starting in the 1980s, payment systems gradually shifted from net systems (where only the net position deriving from incoming and outgoing payments is transferred) to RTGS systems. Net systems by definition require substantially less liquidity compared to RTGS systems, but they also require deferred settlement, which comes with settlement risk.4This may re-introduce credit risk. 5Liquidity-saving mechanisms may follow different approaches, which often involve off-setting algorithms (i.e., matching payments bilaterally or multilaterally and settling them simultaneously). Payment splitting, limits, queues and liquidity reservation may also be applied.