Media contacts

Green Target

The growth of CLSNet, the next best thing after CLSSettlement

As emerging market (EM) currencies continue to outpace the market in terms of growth, the FX market has seen renewed attention towards reducing FX settlement risk. Policymakers and regulators are exploring ways to expand payment-versus-payment (PvP) settlement to currencies for which it is not currently available. This heightened concern about mitigating FX settlement risk has sparked industry discussions about how best to address it.

FX settlement risk is sensitive to today's growing geopolitical challenges as well as market and economic turbulence. Amid this backdrop, market participants are seeking to maximize liquidity and minimize risk in their FX settlement practices. As the industry grapples with these challenges, CLS’s role in managing settlement risk, especially for currencies not eligible for CLSSettlement, becomes increasingly crucial.

Settlement risk remains one of the most significant risks in the FX market today. CLS currently settles 18 of the most actively traded currencies globally, for over 70 settlement members comprising the world’s leading financial institutions and over 35,000 indirect third-party participants.

CLSSettlement is the industry’s settlement risk success story. It was created to mitigate FX settlement risk by providing PvP settlement. PvP ensures the final transfer of a payment in one currency occurs if, and only if, the final transfer of a payment in the counter currency (or currencies) takes place.

Recent CLSSettlement growth statistics demonstrate that CLS is achieving what it set out to do. In 2023, CLS settled an average daily value of USD6.6 trillion of FX payment instructions, and in December, it settled a new daily record of USD16.3 trillion (previous record was USD15.3 trillion on 15 December 2021). A major contributor to this growth has been the asset management community. Asset managers access CLSSettlement via settlement members that provide third-party services, as do other indirect participants like corporates, banks and non-bank financial institutions. Notably, almost 80% of the top 250 investment managers are now settling through CLSSettlement via their custodian banks.1

“CLS’s priority will be to enhance CLSNet’s functionality even further to effectively address settlement risk for EM currencies.”

To gain further insight into the pockets of remaining settlement risk, CLS collaborated with a subset of its settlement members to analyze their FX trades and determine how they were settled. The findings indicated how the market manages settlement risk and the range of mechanisms used to settle FX flows. It showed that around 90% of the settlement risk exposure associated with their FX trades in the 18 CLS-eligible currencies was successfully mitigated via CLSSettlement with full PvP.

Successful settlement risk mitigation has been achieved for CLS-eligible currencies. However, with the growth in EM currency trading, the remaining challenge is to mitigate settlement risk for currencies ineligible for PvP settlement. Given CLS’s systemic importance, adding new currencies to the settlement service is an extended effort that requires ongoing support from the relevant central bank and the industry, and the target jurisdiction’s laws and regulations may need to be changed.

CLS has been exploring ways to expand PvP coverage. However, to achieve progress in this area, public and private sector stakeholders will need to closely collaborate over multiple years to overcome regulatory and geopolitical challenges and arrive at an industry solution.

For now CLS is focusing on enhancing CLSNet, its automated bilateral payment netting calculation service for over 120 currencies. CLSNet helps to mitigate operational risk for EM currency trades. By standardizing and automating the netting calculation process, it facilitates the reduction of payment obligations exposed to settlement risk while improving operational and liquidity efficiencies. Moving forward, CLS’s priority will be to enhance CLSNet’s functionality even further to effectively address settlement risk for EM currencies.

Public policy efforts have focused on the issue of mitigating settlement risk. Building block 9 of the Financial Stability Board’s cross-border roadmap focuses on increased adoption of PvP settlement. The FX Global Code, published by the Global Foreign Exchange Committee, includes key principles concerning settlement risk (principles 35 and 50) that emphasize the use of PvP settlement mechanisms where available and recommend the use of bilateral netting in cases where PvP settlement is not available.

CLSNet supports adherence to these principles, as trade details sent to CLSNet are validated and matched up to the pre-determined cut-off times between counterparties for each currency. This ensures that only confirmed trade details are included in the automated net calculation and that there is a single common record of the net payment obligations. By automating the netting process via a centralized platform, participants benefit from greater operational efficiency and increased risk mitigation for currencies currently unable to settle in CLSSettlement.

CLS believes that the true benefits of the bilateral netting calculation process can only be realized with an industry utility model that is centralized and standardized, underpinned by an underlying rulebook. Crucially, these types of conditions are most likely to produce the network effect, which is essential if such services are to deliver optimal benefits to FX market participants.

“CLSSettlement is doing what it set out to do: mitigate FX settlement risk.”

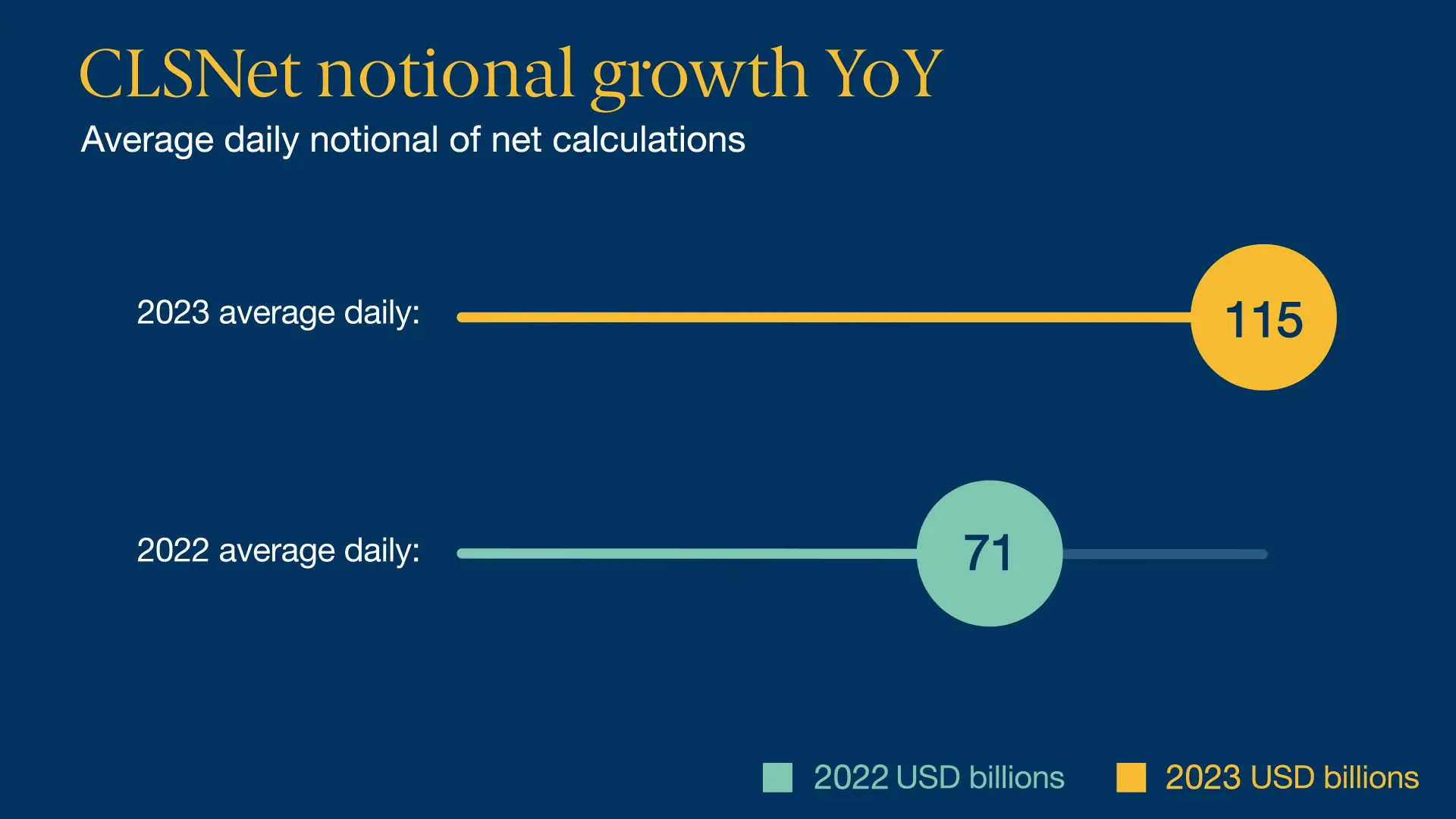

Recent growth statistics illustrate the scale of industry support for CLSNet. The average daily notional value of net calculations in CLSNet consistently exceeded USD115 billion over the last 12 months, and in December 2023 reached a record of USD445 billion netted. The growing CLSNet community already includes eight of the top ten global banks2, and extending the network to more banks, funds, corporates and non-bank financial institutions is a priority for the coming year. CLS is confident that the tangible benefits of the service will continue to drive uptake of the service.

Further, when the US and Canadian securities markets move to T+1 settlement in May 2024, the asset manager community and other market participants will face new challenges with the FX post-trade lifecycle, including time constraints that may limit the use of CLSSettlement. CLSNet can help to reduce funding requirements and payment instructions by calculating net payment obligations that facilitate payment netting.

CLSSettlement is doing what it set out to do: mitigate FX settlement risk. Growth numbers and settlement risk analysis demonstrate the strong industry support for the service. Settlement risk is largely mitigated for CLS-eligible currencies.

With the growth in EM currency trading, the remaining challenge is how best to mitigate risk for currencies ineligible for PvP settlement. For now, we believe this is CLSNet. Recent growth reflects the industry’s support for the service and its need for a centralized, standardized, and automated process that enables them to mitigate operational risk, optimize liquidity and create operational efficiencies. CLS’s role is to continue building the CLSNet community – a key priority for 2024.

First published in e-forex.net, January 2024.